Omnibus SRO Restrictions - Economy | UPSC Learning

Topics

0 topics • 0 completed

🔍

No topics match your search

Omnibus SRO Restrictions

Medium⏱️ 8 min read

economy

📖 Introduction

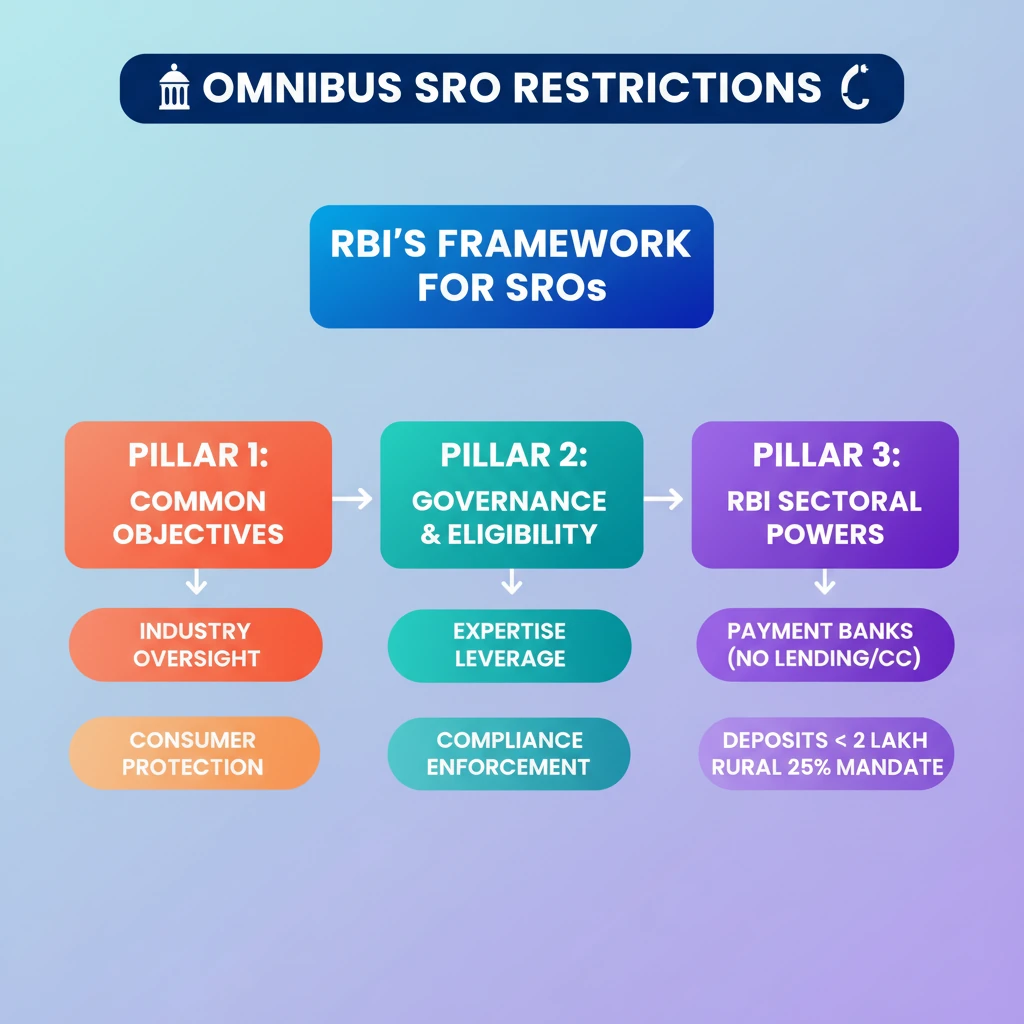

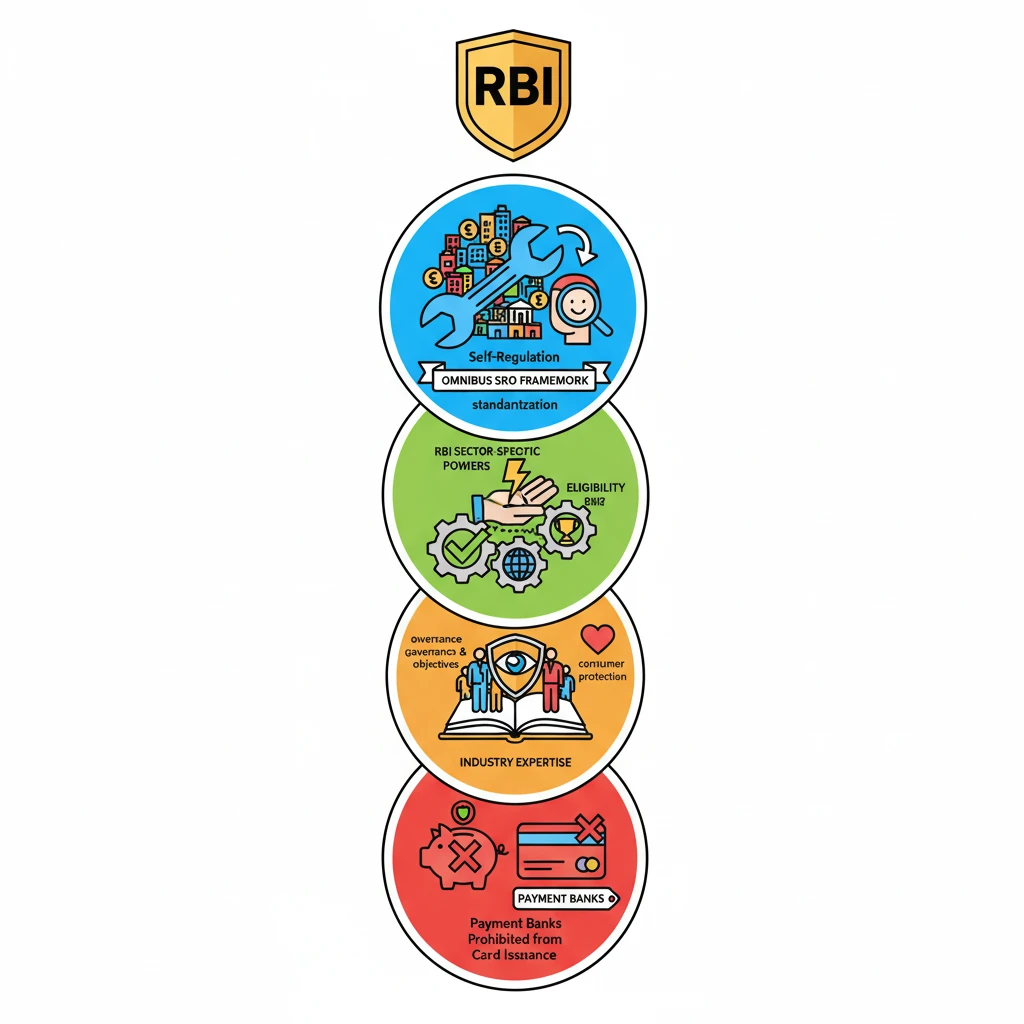

<h4>Understanding the Omnibus SRO Framework</h4><p>The <strong>Reserve Bank of India (RBI)</strong> has recently finalised the <strong>Omnibus Framework for Recognising Self-Regulatory Organisations (SROs)</strong>. This significant move aims to streamline and strengthen the regulatory oversight of its <strong>Regulated Entities (RE)</strong> across various sectors.</p><div class='key-point-box'><p>The <strong>Omnibus Framework</strong> provides a comprehensive set of guidelines and regulations. Its primary goal is to facilitate a coordinated and integrated approach to regulatory oversight, while also allowing for necessary sector-specific guidelines.</p></div><h4>Core Components of the SRO Framework</h4><p>The framework establishes <strong>common objectives</strong>, <strong>functions</strong>, <strong>eligibility criteria</strong>, and <strong>governance standards</strong> for all SROs. These standards apply universally, irrespective of the specific sector an SRO operates within, ensuring a baseline of quality and integrity.</p><p>It also meticulously defines the <strong>membership criteria</strong> and terms for entities wishing to join an SRO. While these represent the minimum requirements set by the <strong>RBI</strong>, recognised SROs are actively encouraged to develop and implement their own best practices, fostering continuous improvement.</p><p>The <strong>Reserve Bank</strong> retains the flexibility to impose <strong>sector-specific additional conditions</strong>. These conditions will be specified when the <strong>RBI</strong> invites applications for the recognition of SROs for particular segments of the financial market.</p><h4>Payment Banks: An Example of RBI's Regulated Entities</h4><p><strong>Payment Banks</strong> are a specific category of <strong>Regulated Entities</strong> under the <strong>RBI's</strong> purview. They operate with a distinct set of restrictions and permitted activities, designed to promote financial inclusion while managing risks.</p><h4>Prohibited Services for Payment Banks</h4><p><strong>Payment Banks</strong> are explicitly prohibited from conducting <strong>lending operations</strong>. This means they cannot provide loans or advances to individuals or businesses. Additionally, they are restricted from issuing <strong>credit cards</strong>.</p><div class='info-box'><p>Due to these prohibitions on lending, <strong>Payment Banks</strong> are also exempt from the <strong>Priority Sector Lending (PSL) regulations</strong>. These regulations typically mandate traditional banks to lend a certain percentage of their funds to specific sectors like agriculture, education, and small businesses.</p></div><h4>Rural Outreach Requirements for Payment Banks</h4><p>To ensure broader financial inclusion, <strong>Payment Banks</strong> have a mandatory <strong>rural outreach requirement</strong>. At least <strong>25%</strong> of a <strong>Payment Bank’s physical access points</strong> must be established in <strong>rural centers</strong>.</p><h4>Major Activities Performed by Payment Banks</h4><ul><li><strong>Accepting Deposits:</strong> They can accept deposits from individuals and small businesses. The current limit is set at <strong>Rs 2 lakh per account</strong>.</li><li><strong>Remittance Services:</strong> Facilitating domestic money transfers and providing efficient remittance services.</li><li><strong>Card Issuance:</strong> Issuing <strong>ATM/Debit cards</strong>, <strong>prepaid payment instruments (PPIs)</strong>, and other electronic payment methods.</li><li><strong>Internet Banking:</strong> Offering comprehensive internet banking services, including online fund transfers and bill payments.</li></ul><div class='exam-tip-box'><p><strong>UPSC Insight:</strong> Understanding the distinct operational model of <strong>Payment Banks</strong> and the rationale behind the <strong>Omnibus SRO Framework</strong> is crucial for GS-III (Economy) and GS-II (Governance). Focus on their role in <strong>financial inclusion</strong> and <strong>regulatory architecture</strong>.</p></div>

💡 Key Takeaways

- •RBI's Omnibus SRO Framework standardises self-regulation for all its Regulated Entities.

- •The framework sets common objectives, governance, and eligibility for SROs, with RBI retaining sector-specific powers.

- •SROs leverage industry expertise for oversight, compliance, and consumer protection.

- •Payment Banks are RBI-regulated entities prohibited from lending and credit card issuance.

- •Payment Banks focus on deposits (up to Rs 2 lakh), remittances, and digital payments, with a 25% rural outreach mandate.

🧠 Memory Techniques

98% Verified Content

📚 Reference Sources

•Reserve Bank of India (RBI) Notifications and Circulars (Omnibus Framework for Recognising Self-Regulatory Organisations for its Regulated Entities)

•Reports of the Committee on Comprehensive Financial Services for Small Businesses and Low-Income Households (Nachiket Mor Committee)